This weekend marked a month since the U.S. and Israel initiated targeted strikes on Iran on 28 February 2026, triggering retaliatory Iranian missile and drone attacks against Israel, Bahrain, Kuwait, Qatar, Oman, Saudi Arabia, the United Arab Emirates (UAE), Iraq, Jordan and Azerbaijan. Lebanon itself has also been the site of military engagements between Israel and Hezbollah. Attacks across the region have generally targeted U.S. military bases, vessels in the Persian Gulf, Strait of Hormuz, and Gulf of Oman (see Deep Dive), diplomatic sites, transport hubs, and critical government and civilian facilities, including energy infrastructure.

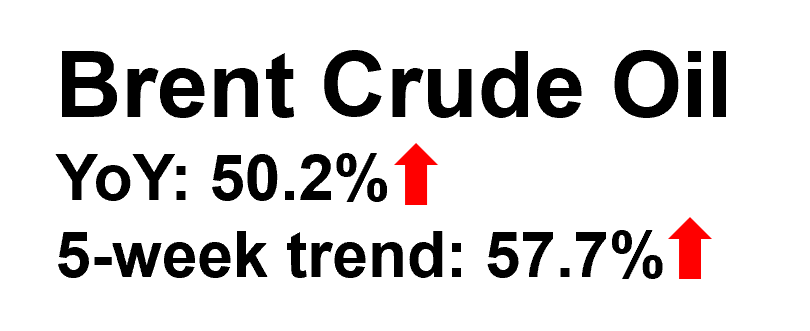

As of 30 March, the situation remains uncertain. Recent comments made by President Donald Trump have struck a more conciliatory tone towards Iran, contributing to hopes of a de-escalation in tensions. However, despite the extension of his deadline for Iran to open the Strait of Hormuz within 10 days to 6 April, developments in parallel suggest the situation could worsen. On 28 March, the Houthis opened up a new front, with missile and drone attacks on Israel. The group, who warned they will escalate pressure on the U.S. and Israel, also threatened to resume maritime attacks. Additionally, the deployment of thousands of Marines and several more battleships and a shift in posture by Saudi Arabia and the UAE towards supporting military action against Iran suggest the war could yet escalate further. According to reports from the French government, 30 to 40 percent of Gulf refining capacity has been impacted. This presents substantial long-term implications for global oil refining operations and supply, even if a ceasefire is reached within the next few weeks.

Over the past decade, major global crises have presented various socio-economic challenges to Africa. Whereas the COVID-19 pandemic placed the continent’s healthcare systems under pressure, the Russia-Ukraine war exposed levels of food insecurity. The current Middle East crisis could be more severe. While the impact on the continent is likely to be multi-fold, this Deep Dive explores the impact of shortages and price hikes of key commodities – namely refined petroleum products, nitrogenous fertiliser and food imports.

Oil Supply Disruptions and Energy Insecurity

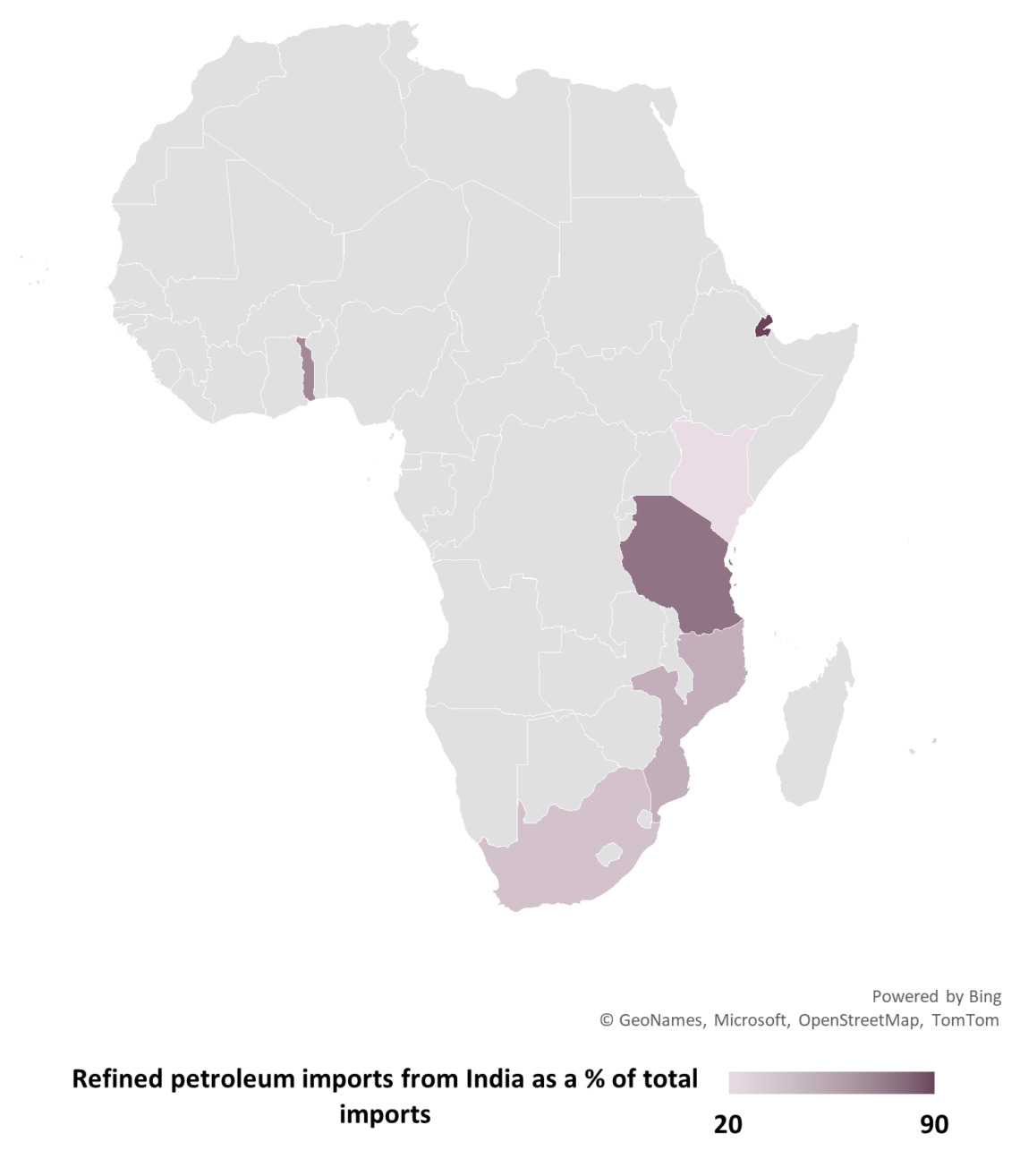

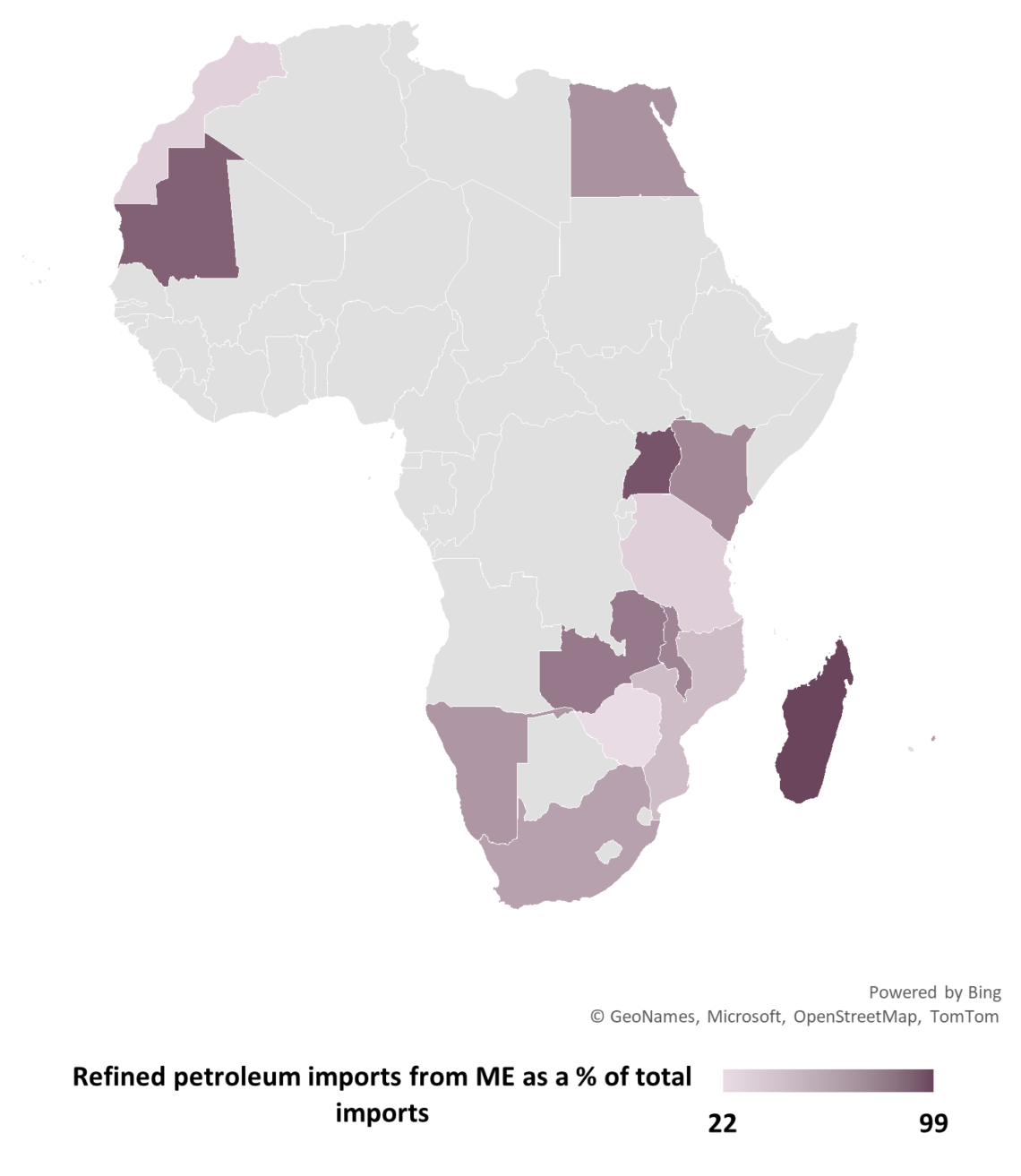

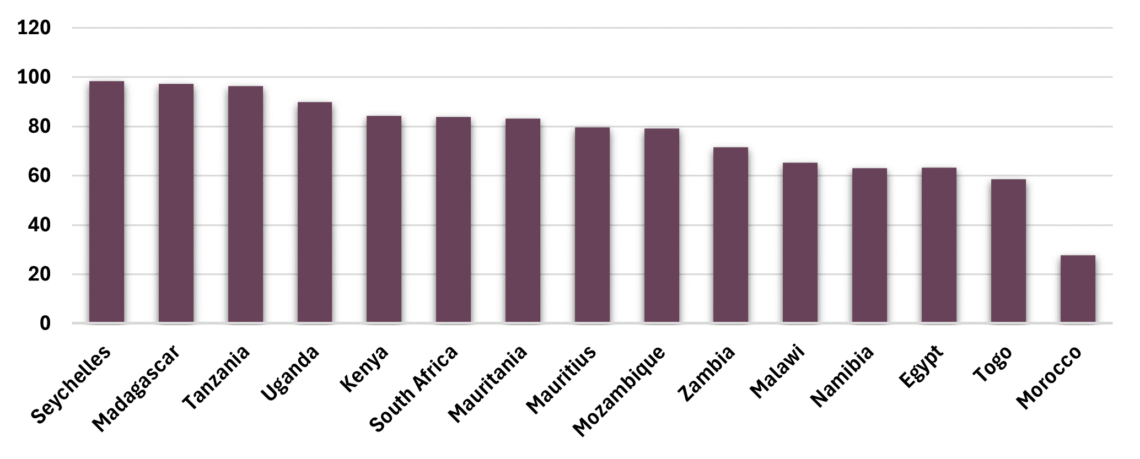

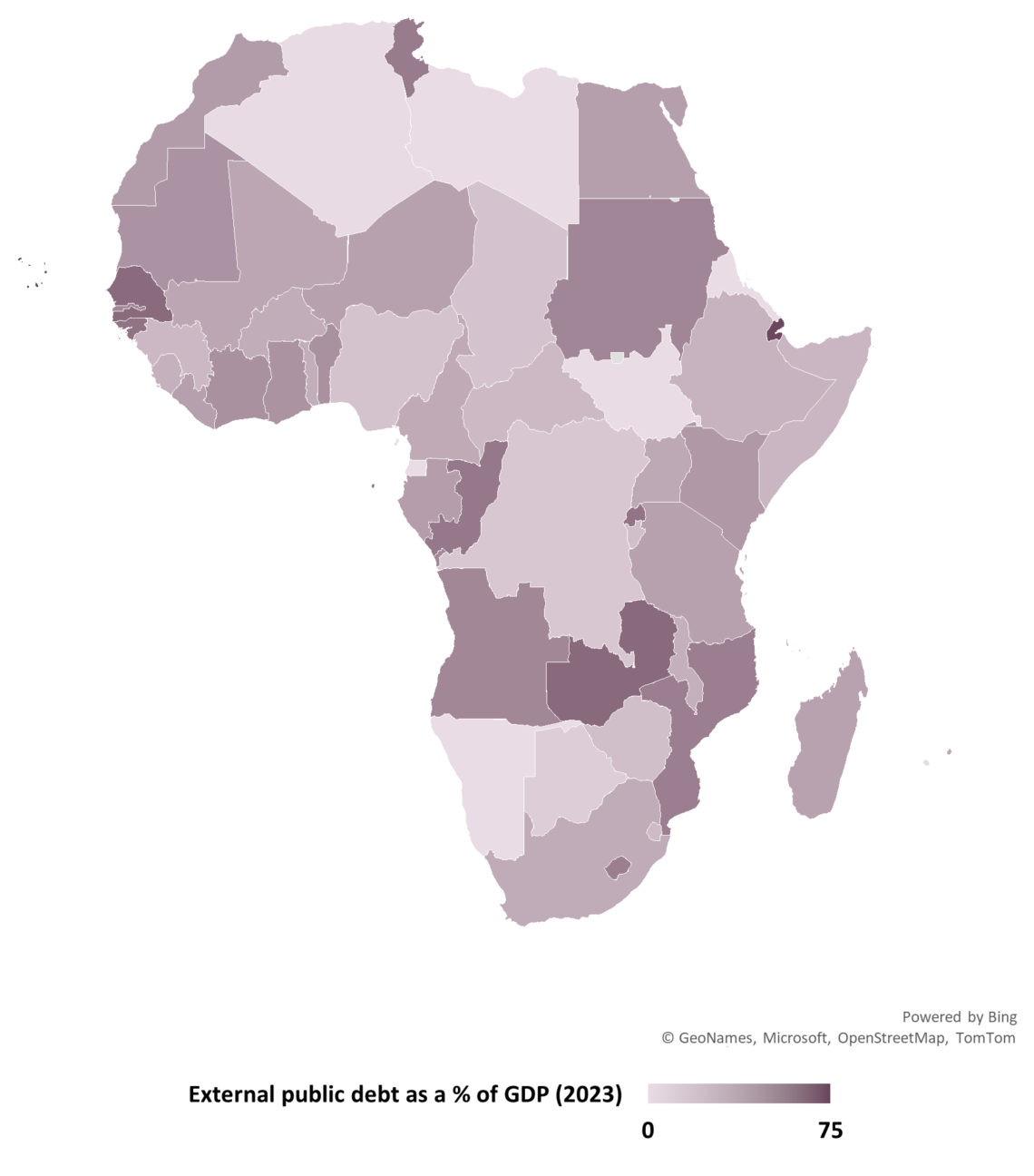

While all African countries are likely to face fuel supply challenges, countries in Southern and Eastern Africa will remain the most vulnerable to pressing supply shortages as a result of the conflict. Moreover, countries reliant on Asian refined petroleum exports will also be impacted as a secondary or additional effect. Oman, Saudi Arabia, and the UAE are key exporters of refined petroleum to Eastern and Southern Africa. The conflict has directly affected the ability of these countries to export refined petroleum to their African trading partners through the Strait of Hormuz. The conflict has also led to the disruption of crude oil supplies to China, South Korea and India, the latter being a key source of refined petroleum for Africa. As a result, African nations that depend on Asian countries for refined petroleum may also encounter difficulties in maintaining consistent supply. All three countries have directed refiners and traders to focus on ensuring domestic demand is met before meeting external obligations. Within Africa, infrastructural limitations, such as a reliance on road-based distribution of fuel and a lack of storage, pipeline and port infrastructure, are also factors affecting countries’ vulnerability and exposure to the impact of fuel shortages, particularly in landlocked, low-income countries and those affected by conflict, notably Sudan, South Sudan, Mali and Burkina Faso, where the presence of armed groups also hinders distribution. The below graphics detail which countries remain the most vulnerable in this regard.

Agricultural Shocks and Food Security Implications

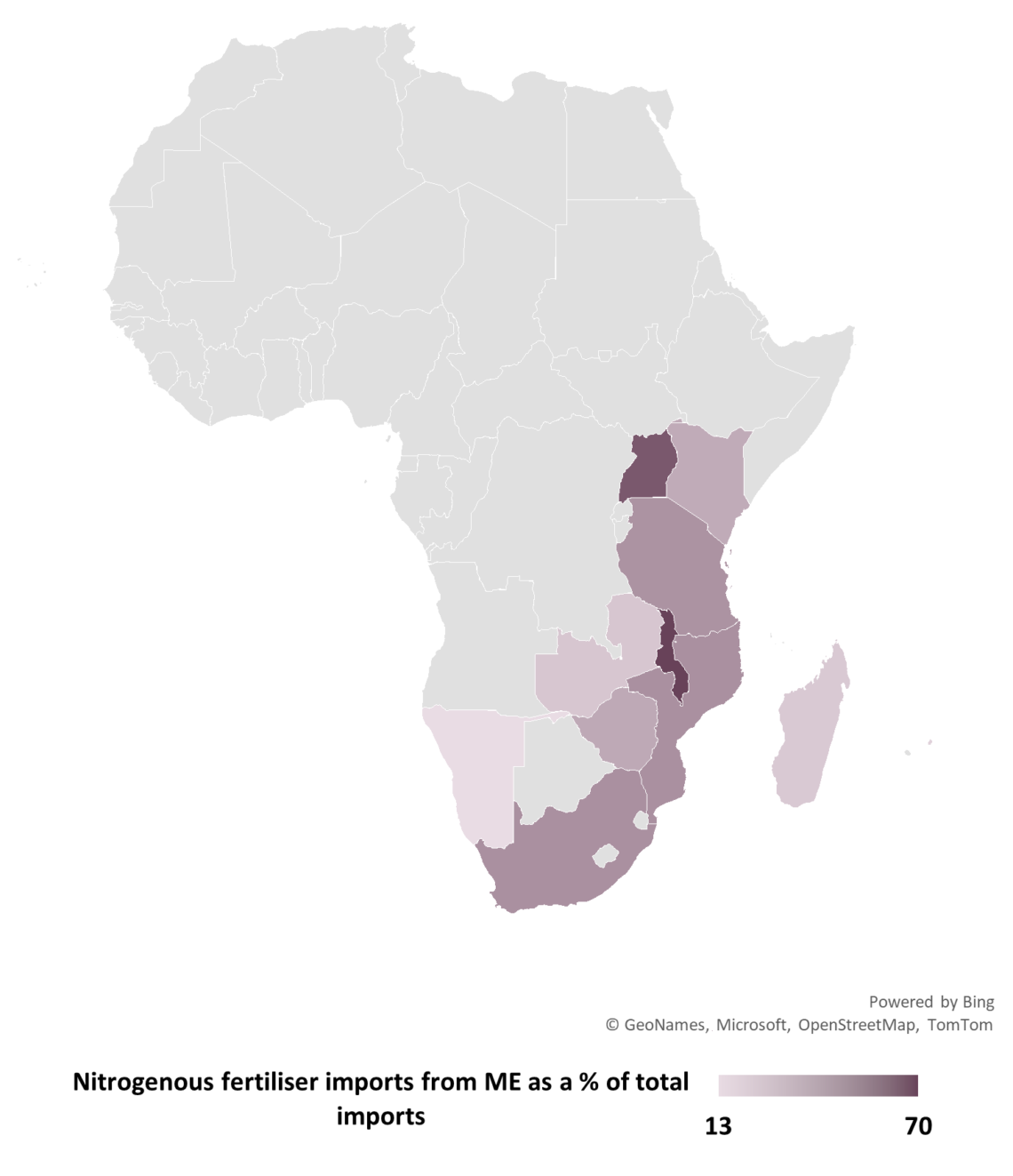

Shortages of nitrogenous fertilisers and sulphur are likely to have a direct impact on food production in Africa. Saudi Arabia, Oman, the UAE, Qatar and Bahrain together exported almost 10 percent of all fertilisers globally in 2024. Crucially, Saudi Arabia, Oman, the UAE, Qatar and Bahrain together accounted for almost 19 percent of all nitrogenous fertiliser exported globally in 2024, according to analysis of data from Harvard’s Atlas of Economic Complexity. Together, all five countries account for a total of 21 percent of Africa’s nitrogenous fertiliser imports. Key importers include Kenya, Mozambique, Malawi, Uganda, Zambia and South Africa, who are likely to remain the most vulnerable. Nitrogenous fertilisers, used to grow crops such as maize, wheat, rapeseed, and some fruits and vegetables, play an essential role in crop yields. Other key exports to the region include sulphur, with the Middle East accounting for nearly 50 percent of global sulphur trade. Sulphur is a key raw material for the production of phosphatic fertiliser, which is important for higher crop quality.

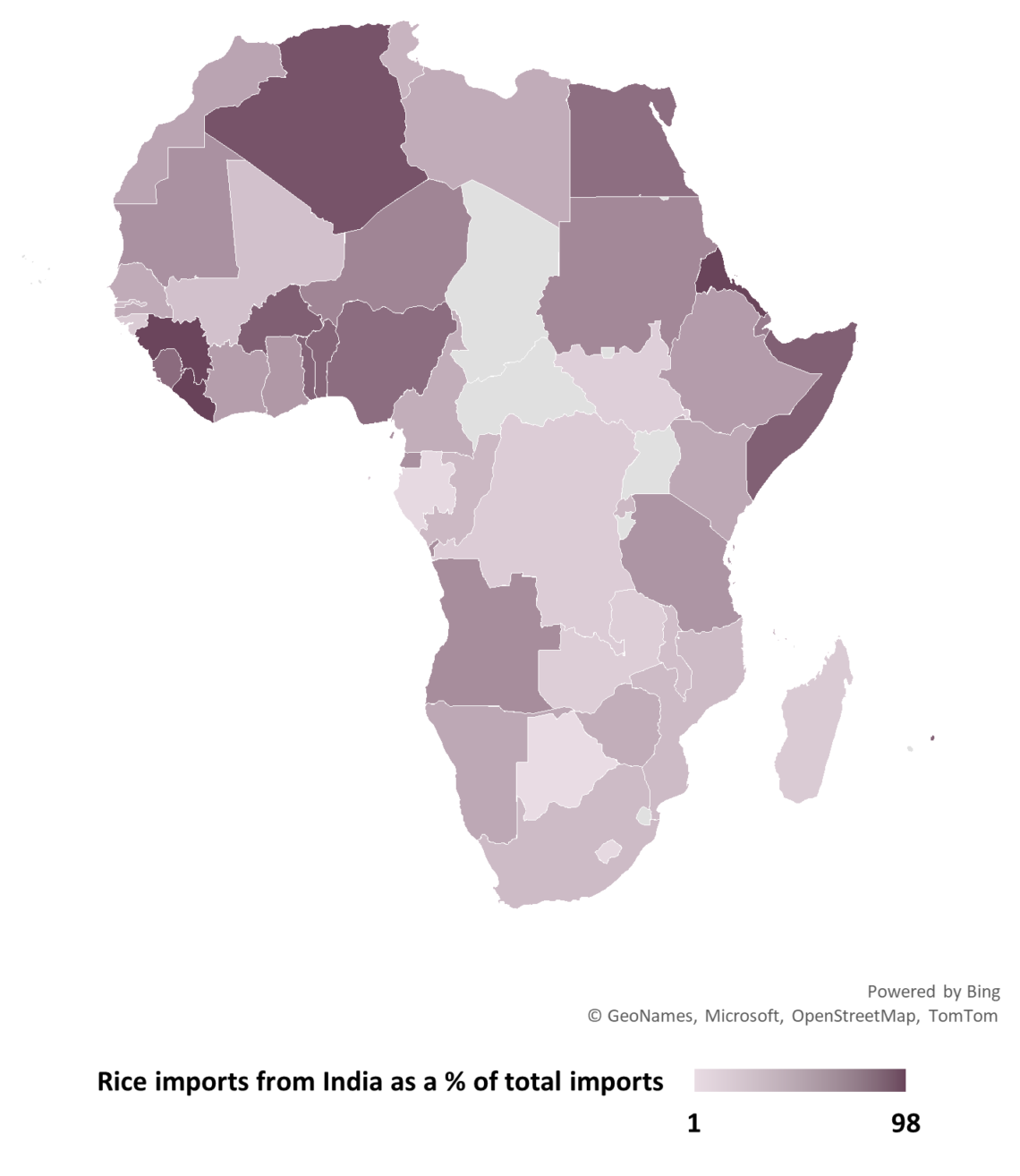

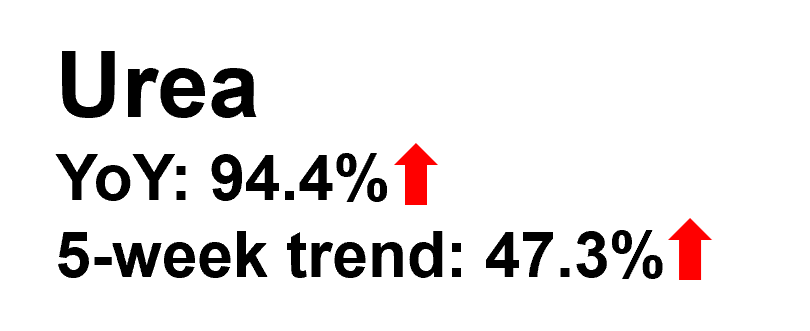

Secondary impacts through reduced or higher prices for food imports are also likely to take hold in the coming weeks. India, the U.S., Australia, Brazil, France, and Turkey are the major importers of nitrogenous fertiliser worldwide. In 2024, India and Brazil accounted for approximately 24 percent of Africa’s cereal imports. Consequently, any challenges these countries encounter will affect their main African trading partners, resulting not only in shortages but also in higher prices. Given that supply shortages have impacted fertiliser exports through the Strait of Hormuz, prices of urea have risen exponentially. The price is also linked to liquefied natural gas (LNG), used by countries such as India to operate domestic urea plants. Approximately 75 percent of India’s petroleum gas imports transited through the Strait of Hormuz in 2024. Therefore, the throttling of LNG and nitrogenous fertiliser imports will likely affect both the supply of Indian exports and the prices of these exports to Africa. Key Indian agricultural commodity exports, particularly rice, remain a key concern with countries in West Africa most at risk. Other countries such as Thailand, Pakistan and Vietnam, among the countries worst affected globally, are also key exporters of rice to Africa. Moreover, given the increasing regionalisation of trade across Africa, countries such as Uganda, eSwatini, Ethiopia, the DRC, Lesotho, Zimbabwe, and Botswana – which rely on rice and/or nitrogenous fertiliser imports from regional suppliers like Tanzania, Kenya, South Africa, and Zambia – are also likely to be significantly impacted, despite having no direct dependence on Middle Eastern imports.

Assessment

Amid rising global oil prices, import-dependent countries, particularly those reliant on petroleum imports, will face inflationary pressures, with southern and eastern African nations especially affected. Rising transport costs driven by the conflict in Iran are likely to be passed on to consumers, contributing to higher inflation and reducing purchasing power.

Over the longer term, low income and lower-middle income countries face major challenges in sustaining or implementing policies or measures aimed at reducing the inflationary impact of the crisis, such as fuel subsidies. Furthermore, countries reliant on energy imports, and other essential imports such as fertiliser, face currency devaluation challenges. Low foreign exchange reserves, external debt obligations, and investors moving assets to more secure markets are compounding factors. The extent of currency devaluation is likely to increase as the duration of the Iran conflict persists. Oil producing countries face the lowest risk of currency devaluation.

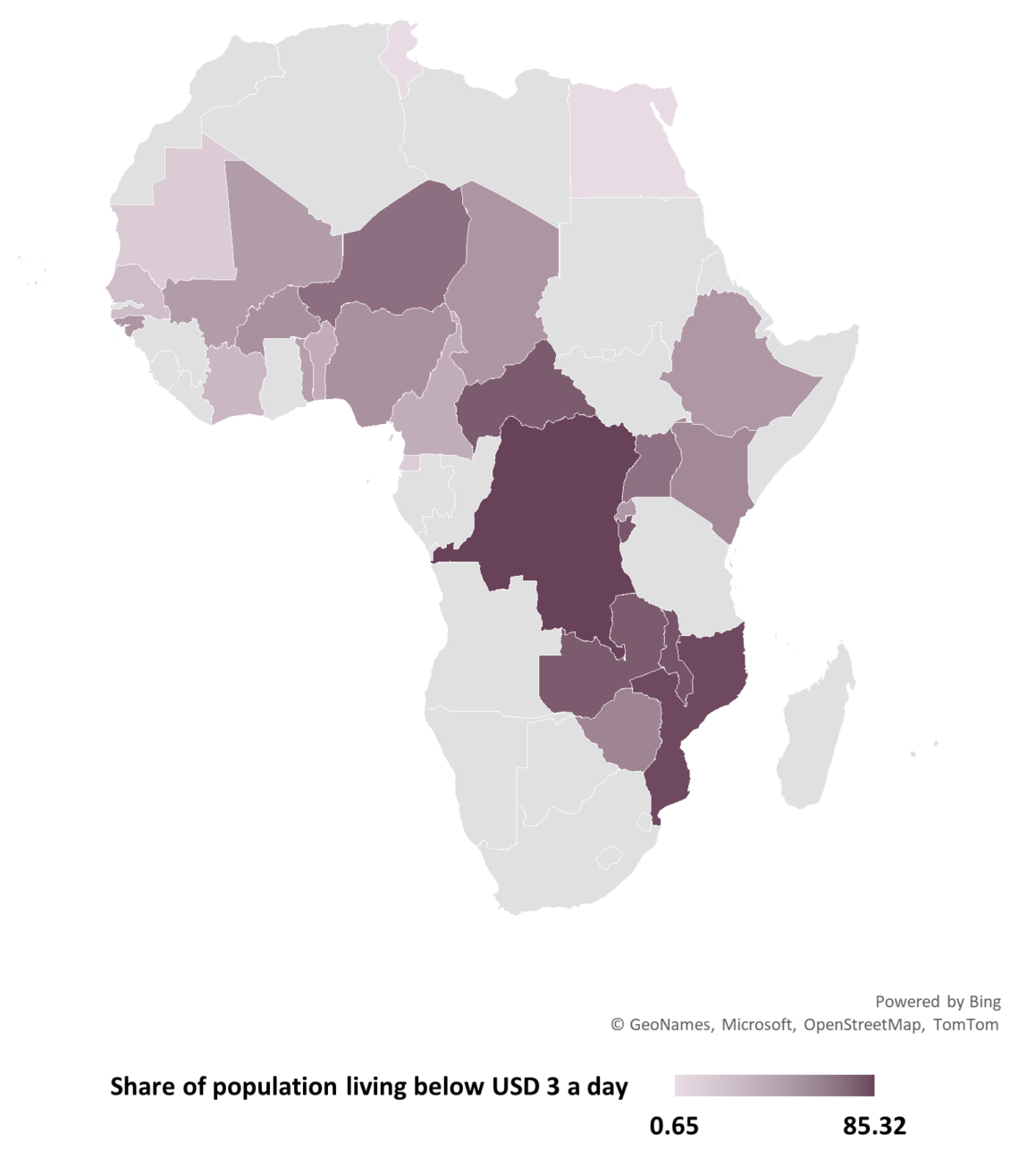

The incidence of civil unrest across Africa is expected to increase over the short term in response to these inflationary pressures. Low income and lower-middle income countries will face major challenges in sustaining or implementing policies or measures aimed at reducing the inflationary impact of the crisis, such as through fuel subsidies. These countries remain at risk of cost-of-living unrest. Indeed, civil disorder risks are broadly higher in low-income countries and in countries with substantial numbers of the population living below the International Poverty Line (less than USD 3 per day). At the same time, countries that have recorded high levels of anti-government sentiment over the past 12 months, such as Morocco, Kenya, Madagascar, Tanzania, Angola, Cameroon and Mozambique, face an increased risk of intense civil disorder as well, while a strong protest culture in countries such as Nigeria, South Africa, Ivory Coast and Guinea is also likely to galvanise local populations on the streets. Elections in over a dozen countries this year, particularly Benin, Cape Verde, Ethiopia, Gambia, Somalia and Zambia, coupled with challenging socio-economic conditions, may further result in particularly intense street protests and unrest before, during and after the election period. In contrast, those countries operating under more centralised systems of governance, including Rwanda, Mali, Burkina Faso and Niger, are likely to experience reduced civil disorder alongside heightened repression and the enforcement of strict measures such as curfews.

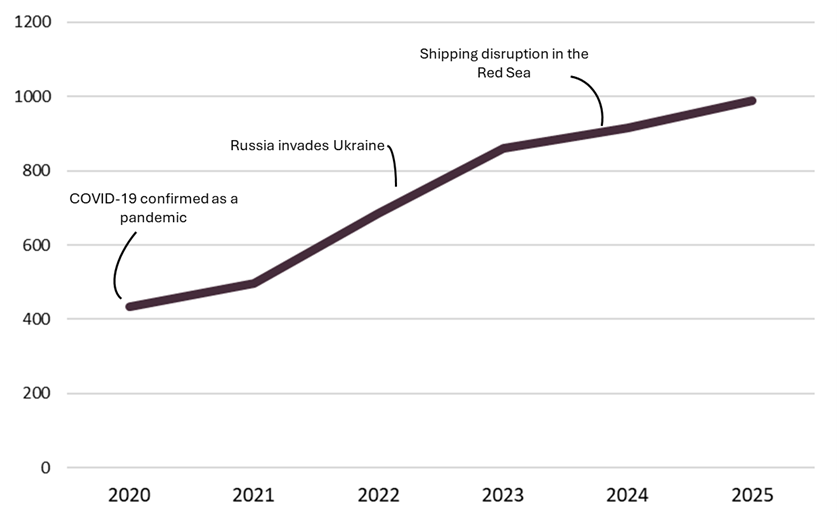

Data: UNCTAD

Given limited amounts of fuel reserves held by countries in Africa, shortages and fuel rationing are highly likely in certain markets, as is insecurity related to this key commodity. While many countries will likely introduce subsidies to absorb inflationary impacts, restrictions on fuel use will need to be in place to manage supply constraints. In Ethiopia, the government has already introduced emergency fuel subsidies. In South Africa, some fuel stations have imposed limits on the amount of fuel sold per customer, while in Kenya, independent retailers have reported dwindling supplies. Businesses in countries like the DRC, as well as landlocked nations such as Ethiopia, Malawi, and Zambia, are expected to encounter higher operational expenses and potential fuel shortages. This is largely due to the dependency on road-based fuel transportation throughout much of Africa and the challenges posed by limited road infrastructure. Country-specific challenges are also highly likely to emerge. For instance, taxi violence may rise in South Africa owing to the impact operating costs will have on competition. Meanwhile, the incidence of oil and fuel theft will almost certainly rise in oil-producing/refining countries like Nigeria, Libya, Angola and South Africa, given the rise in regional demand.

Countries dependent on oil for electricity generation may resort to impose load shedding or limit non-essential usage. Countries have already begun to implement such measures. For instance, on 25 March, Mauritius implemented restrictions including curbs on grid power for non-essential uses such as decorative lighting, swimming pool heating and fountains. The government is increasing the use of alternative sources of energy, such as charcoal and may restrict electricity use in high-consumption areas, such as shopping malls, football grounds at night and schools after hours. Similarly, South Sudan implemented rotational load shedding to manage available fuel reserves.

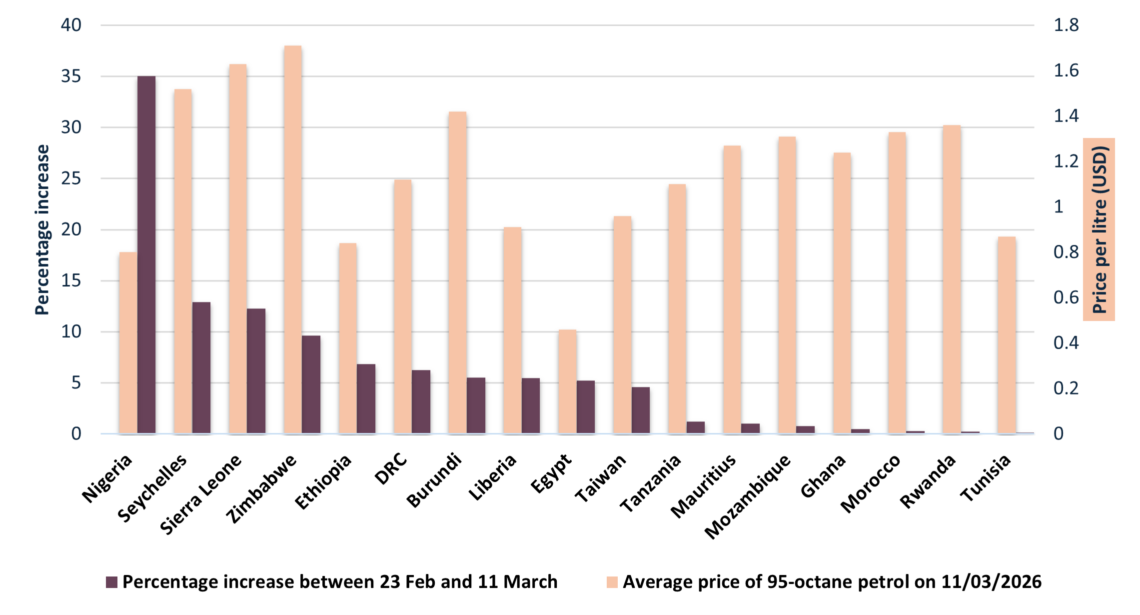

Higher fuel prices and potential shortages will also impact the aviation sector, having a knock on effect to other crucial sectors, like tourism. Nearly 70 percent of jet fuel and kerosene imported by Africa transits the Strait of Hormuz, according to S&P Global via Reuters. Airlines in Africa already spend approximately 10 to 30 percent more than the global average on fuel costs, therefore operating expenses are likely to rise significantly. Moreover, logistical constraints mean airlines operating in landlocked countries, where fuel takes longer to arrive, will likely see higher operating costs. International airlines, such as Air France-KLM, have increased the price of its economy class tickets by EUR 50. Similar measures are likely to be imposed by other airline carriers, which will have a detrimental effect on countries’ tourism sectors.

Although nitrogenous fertiliser is not widely used across Africa compared to other regions, given global supply shortages, food shortages are high likely for African countries dependent on imports of not only cereals like rice, but also grains from Europe. Prices of other fertilisers, such as di-ammonium phosphate, have also increased; however, the rising cost and shortages of nitrogenous fertilisers are more significant, as it is the most essential type of fertiliser used every season. Farmers in the Northern Hemisphere are set to begin fertilising their fields, and current shortages are likely to result in not only lower yields but also potential crop failures in the next season. Market dynamics are also a factor: although fertiliser prices remain below the peaks following Russia’s invasion of Ukraine in 2022, grain prices have since declined. As a result, tighter profit margins may prompt farmers to switch to less fertiliser-intensive crops or reduce application rates, potentially lowering yields. Lower yields in turn will likely lead to higher consumer prices.

About Castor Vali Security Information Services

This deep dive forms part of Castor Vali’s wider Africa intelligence and risk monitoring capability. While this report provides detailed analysis of the escalation in the Middle East and the ripple effects across Africa, our ongoing monitoring ensures that clients receive timely, operationally relevant updates as security dynamics continue to develop.

Our Africa risk monitoring service is designed to help organisations operating across the continent remain informed of emerging threats, including terrorism, political instability, civil unrest, organised crime, and wider geopolitical developments that may affect personnel, infrastructure and commercial operations. Through continuous analysis of local reporting, incident data and regional dynamics, we provide strategic insight that supports informed decision-making and effective risk mitigation.

Africa intelligence subscriptions provide access to:

- Daily Briefs – weekday summaries of key political, security and socio-economic developments across African markets.

- Real-Time Alerts – notifications of major incidents delivered via email and mobile, including analysis, advice and mapping where relevant.

- Weekly Reports – structured reviews of significant events supported by visual data, graphics and incident mapping.

- Monthly Reports – high-level country assessments with short to medium-term risk ratings and forward-looking analysis.

- Deep Dives – detailed examinations of emerging trends, security threats and political developments affecting specific regions or sectors.

We welcome enquiries from organisations seeking to strengthen their situational awareness across Africa. Complimentary trials are available for companies wishing to evaluate the service.

To explore our Africa intelligence reporting or request trial access, please complete the sign-up form below.

Security Information Service Trial

Clients interested in trailing our subscription packages should complete this form: